Published On:

February 4, 2026

Updated On:

February 4, 2026

Navigating the Indian real estate market as a Non-Resident Indian (NRI) requires a firm grasp of FEMA regulations, tax liabilities, and repatriation limits. This comprehensive guide breaks down the 2025-26 rules for buying, selling, and renting property in India, ensuring your investment journey is legally compliant and financially optimized.

For millions of Non-Resident Indians (NRIs), owning a piece of land in India is more than just a financial decision; it is an emotional anchor to their roots. Whether you are looking to buy a retirement home, sell an ancestral property, or manage rental yields from afar, the Indian real estate landscape offers immense potential. However, it also comes with a unique set of regulatory hoops managed by the Foreign Exchange Management Act (FEMA) and the Income Tax Act.

With recent updates in the Union Budget 2026-27 simplifying compliance for buyers and altering capital gains structures, the landscape has shifted. This guide serves as your comprehensive in-house manual to navigating property transactions in India, ensuring you maximize returns while staying on the right side of the law.

The first step for any NRI investor is understanding the "permitted list" of assets. FEMA guidelines are quite specific about the types of properties non-residents can acquire.

As an NRI or an Overseas Citizen of India (OCI), you have a "general permission" to purchase:

The "negative list" is strict. NRIs cannot purchase:

The Reserve Bank of India (RBI) restricts these to protect India's agricultural sector from speculative foreign investment. However, there is a crucial exception: Inheritance. If you inherit agricultural land from a resident Indian, you are legally allowed to hold it. You just cannot go out and buy it on the open market.

You cannot simply swipe a foreign credit card to buy a flat in Delhi. All transactions must be routed through authorized banking channels. You can pay using:

Pro Tip: Avoid paying in cash or traveller’s cheques. These are strictly prohibited for property transactions and can lead to severe penalties under FEMA.

Selling property as an NRI involves more paperwork than buying, primarily due to tax implications.

Once you sell, the biggest question is: "How do I get my money back to my country of residence?"

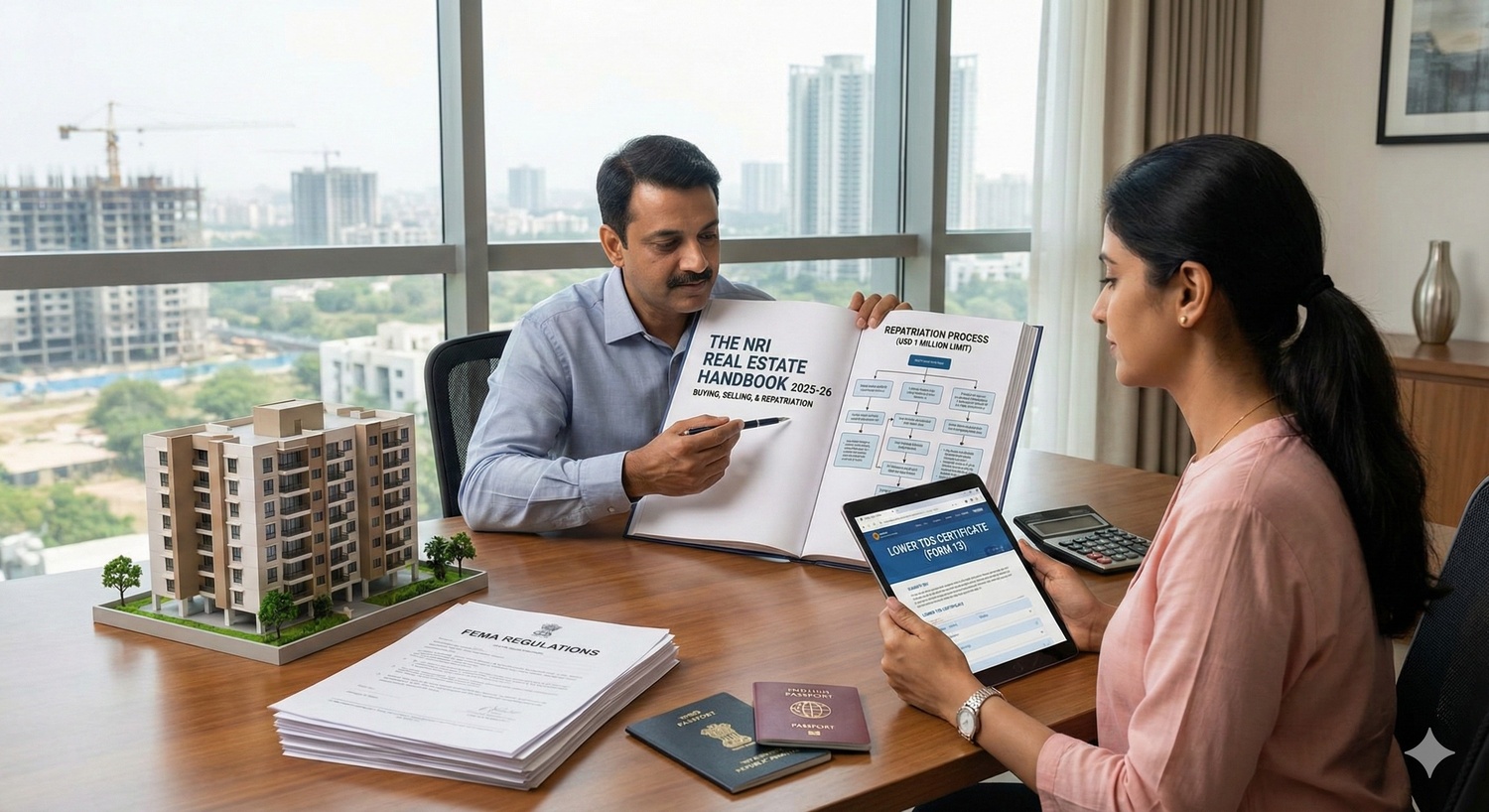

Under current FEMA rules, you can repatriate up to USD 1 million per financial year (April to March) from your NRO account. This limit includes sale proceeds from property, rental income, and other assets.

For residential properties, there is a specific clause regarding the repatriation of the principal amount (the amount you originally invested in foreign currency). You are allowed to fully repatriate the sale proceeds of up to two residential properties. For any property beyond the second one, the proceeds must effectively be credited to your NRO account and are subject to the USD 1 million annual cap.

This is where most NRI sellers face friction. When you sell property in India, the buyer is legally required to deduct tax at source (TDS). Unlike resident sellers where TDS is a flat 1%, for NRIs, the TDS rate is significantly higher because it attempts to cover the potential Capital Gains Tax.

The Cash Flow Problem:Often, the TDS deducted (e.g., 20-23% of the total sale value) is much higher than your actual tax liability (which is calculated on the profit only). This locks up your capital until you file a tax return and claim a refund.

The Solution: Lower TDS Certificate: To avoid this cash flow crunch, you can apply for a Lower Deduction Certificate (Form 13) before the sale is registered. You submit your capital gains calculations to the Income Tax Department, and if satisfied, they issue a certificate authorizing the buyer to deduct tax at a lower rate (e.g., 3% or 5%) instead of the standard 20%.

The taxation on capital gains underwent a major shift in recent budgets.

The Union Budget 2026-27 introduced a critical procedural relief that impacts every NRI seller.

Previously, a resident buying property from an NRI was required to obtain a Tax Deduction and Collection Account Number (TAN) to deduct TDS. This was a massive compliance burden for ordinary buyers, often discouraging them from buying NRI properties.

The New Rule:Effective from late 2026, resident buyers no longer need a TAN. They can deduct and deposit the TDS using just their PAN (Permanent Account Number). This seemingly small change significantly improves the liquidity of NRI-held properties, as it makes the process less intimidating for local buyers.

If you are not selling but renting out your property, the rules are straightforward but strict.

Since you cannot always travel to India for every signature, executing a specific Power of Attorney to a trusted relative or legal professional is crucial. Ensure this PoA is "adjudicated" (registered) in India to be legally valid for property transactions.

While Aadhaar is not mandatory for NRIs, possessing a PAN card is non-negotiable for property transactions. Ensure your KYC status is updated to "Non-Resident" across your bank accounts to avoid the freezing of assets.

If you plan to sell a high-value property worth more than USD 1 million (approx. ₹8-9 Crores), you cannot repatriate the entire amount in a single year. You will need to spread the repatriation over two or more financial years or seek special permission from the RBI, which is granted on a case-by-case basis.

India has DTAA treaties with over 90 countries (including the USA, UK, Canada, and UAE). This ensures you do not pay tax on the same income twice. If you pay Capital Gains Tax in India, you can usually claim a tax credit for that amount in your country of residence, depending on local laws.

The Indian real estate market in 2026 is more regulated, transparent, and accessible for NRIs than ever before. While the inability to buy agricultural land remains a hard stop, the avenues for residential and commercial investment are wide open.

The key to a successful investment lies in the details: funding the purchase correctly through NRE/NRO channels, applying for a Lower TDS Certificate when selling to preserve your liquidity, and understanding the new PAN-based TDS rules to find buyers easily. By adhering to these FEMA and tax guidelines, you can ensure that your property back home remains a source of wealth and connection, rather than a source of legal stress.