Published On:

March 2, 2026

Updated On:

March 2, 2026

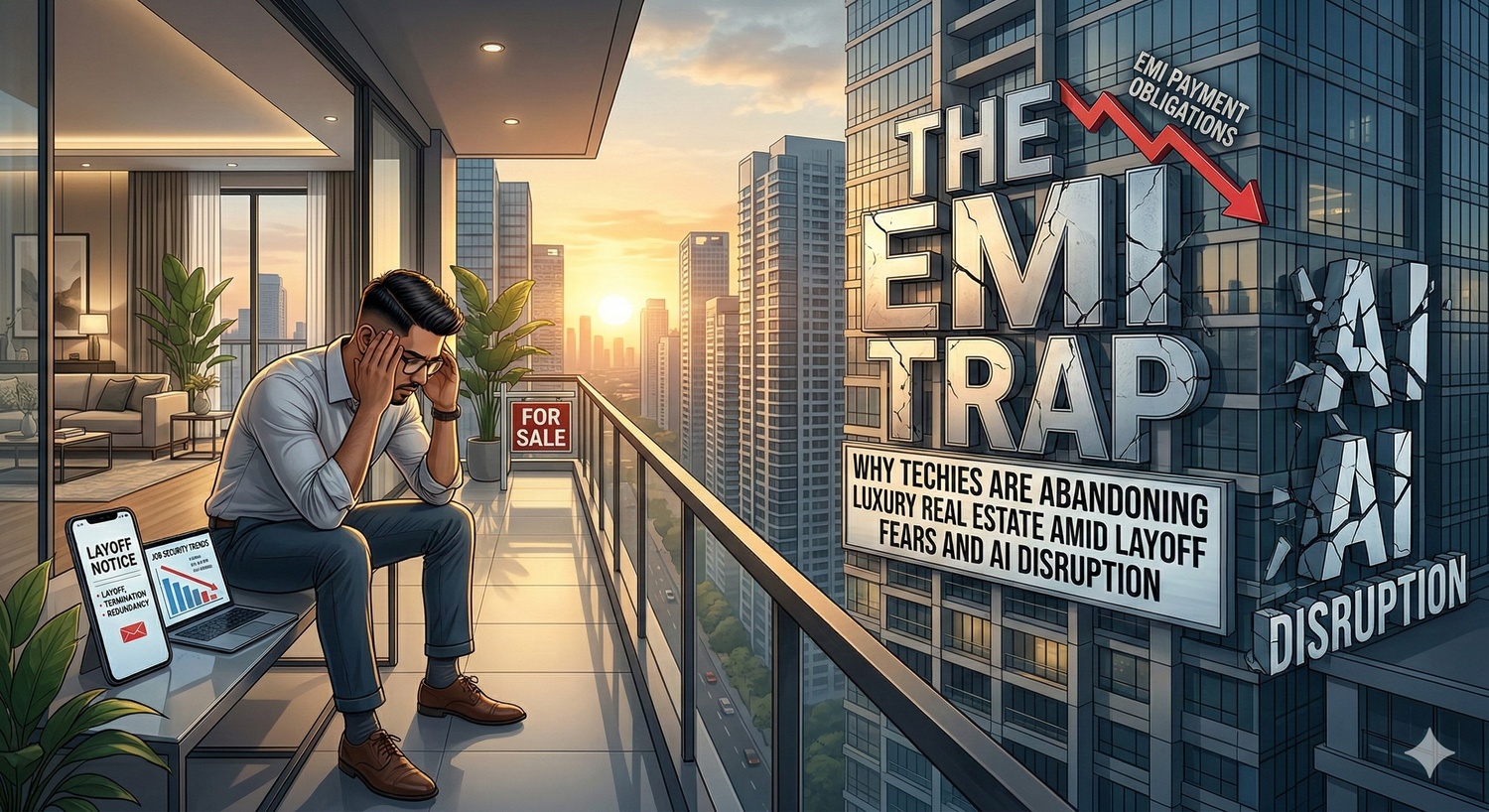

Mounting job insecurity and AI-driven tech layoffs are pushing IT professionals to rethink massive home loans, prompting a shift away from luxury real estate toward renting and financial liquidity. This cautious approach is reshaping property markets in major tech hubs as buyers prioritize survival over lifestyle inflation.

The atmosphere inside the glittering corporate parks of India’s biggest tech hubs has noticeably shifted. For years, the narrative driving the IT sector was one of boundless optimism, characterized by rapid promotions, hefty joining bonuses, and the swift acquisition of premium real estate. Buying a luxury apartment in Bengaluru, Hyderabad, Pune, or Gurugram was considered the ultimate rite of passage for a successful software engineer. Today, that enthusiasm has been replaced by a quiet, pervasive anxiety. As artificial intelligence fundamentally reshapes the future of white-collar work and massive corporate restructuring leads to continuous hiring freezes and job cuts, a single, uncomfortable question is keeping many awake at night: what happens to the lifestyle I have built if I lose my job tomorrow?

This growing unease is fundamentally altering how salaried professionals approach long-term financial commitments. The traditional dream of locking into a twenty-year mortgage for a multi-crore home is rapidly losing its appeal. Instead of debating which premium gated community offers the best amenities, tech workers are now calculating their financial runways, questioning the logic of massive debt, and increasingly prioritizing liquidity over homeownership.

To understand the current crisis of confidence, it is necessary to look at the financial behaviors that defined the tech industry’s post-pandemic boom. Between 2021 and 2023, record-high salaries and a surge in remote work drove an unprecedented real estate rally. Developers catered to this newly flush demographic by launching expansive, high-end projects.

Many professionals, assuming their income trajectories would only point upward, aggressively upgraded their lifestyles. They committed to sprawling apartments priced upwards of two or three crores, financed brand-new luxury cars, and took on high-interest personal loans to fund premium interiors and international vacations. It became increasingly common for mid-level engineers to service monthly home loan EMIs exceeding one lakh rupees.

In a stable economic environment, these high monthly outgoings might be manageable. However, personal finance hinges entirely on continuous cash flow. The foundational flaw in this high-leverage lifestyle is that it assumes the money will never stop. When a household’s fixed expenses consume the vast majority of its monthly income, it leaves practically zero margin for error. The moment the salary disappears, the financial architecture collapses almost instantly.

The fear of job loss is not merely theoretical; it is playing out in real time across major IT corridors. The transition from a comfortable corporate life to financial distress can happen with terrifying speed.

Consider the mechanics of a modern home loan. Financial institutions operate strictly on repayment schedules, and the legal frameworks empowering them to recover bad debts are incredibly robust. If a borrower loses their job and subsequently misses just three consecutive EMI payments, the lender can initiate recovery proceedings. Under current financial recovery laws, banks do not require lengthy court interventions to seize and auction a property.

There are increasingly common instances where professionals, after years of diligent payments, have lost their homes entirely due to a sudden layoff. In these distressed auction scenarios, properties are often sold below market value simply to recover the outstanding loan amount. The original buyer is left with nothing but a fraction of their initial investment, completely wiping out years of hard-earned equity. This stark reality serves as a grim warning to the broader workforce: owning a home with a massive mortgage is not a safety net; it is an immense liability if the primary income source is compromised.

What makes the current wave of job insecurity different from previous economic downturns is the underlying cause. Past tech slumps were largely cyclical, driven by global recessions or temporary spending pullbacks. The current environment, however, is being heavily influenced by structural changes, most notably the rapid advancement of artificial intelligence and automation.

Companies are no longer just trimming the fat; they are rethinking how work is executed. Roles that were previously considered entirely secure—ranging from data analysis and quality assurance to basic coding and digital design—are facing unprecedented disruption. Corporate boards are heavily prioritizing capital expenditure on AI infrastructure, effectively forcing management to aggressively control traditional payroll expenses.

This means that a laid-off professional cannot simply walk across the street to a competitor and secure a similar role with a matching salary. The hiring cycles are significantly longer, the technical interviews are far more rigorous, and compensation packages are being heavily rationalized. Committing to a massive, decades-long financial obligation is fundamentally incompatible with an employment landscape where the next five years of a career are entirely unpredictable.

This widespread realization is causing a massive behavioral shift in the housing market. Real estate markets in tech-heavy micro-markets are witnessing a noticeable drop in inquiries and conversions. Projects that would have sold out in weeks just a year ago are now seeing slower absorption rates.

Prospective buyers are aggressively hitting the pause button. Many who had recently paid booking amounts for luxury apartments are choosing to forfeit their initial deposits rather than proceed with the registration and take on a multi-crore debt burden. The mental peace of remaining debt-free is vastly outweighing the desire for a premium address.

Those who are still in the market are drastically altering their budgets. Instead of stretching their finances to the absolute limit to secure a luxury home, buyers are actively seeking out modest, functional apartments in the more affordable brackets. The new financial strategy is to keep the monthly EMI as close to the prevailing rental rates as possible. If a layoff occurs, an EMI that mirrors standard rent is far easier to manage through emergency savings than a bloated six-figure mortgage payment.

Furthermore, existing homeowners are re-evaluating their portfolios. Professionals who purchased second or third properties purely for investment purposes are increasingly choosing to liquidate these assets. They are willing to accept slightly lower capital gains in exchange for immediate liquidity, recognizing that cash in the bank offers far more protection during an employment crisis than a vacant apartment tied to a heavy loan.

The crushing cost of living in primary tech hubs is also driving a geographic dispersion of the workforce. When a household is spending a massive premium on rent, maintenance, domestic help, and daily commutes, a job loss quickly drains even substantial emergency funds.

To stretch their financial runways, many tech workers who have the flexibility of remote or hybrid roles are relocating back to tier-two and tier-three cities. The financial mathematics behind this move are compelling. The cost of living in smaller towns is often a fraction of what it takes to survive in a major metro. By eliminating exorbitant city rents and inflated lifestyle costs, professionals can effectively triple or quadruple the lifespan of their savings. A financial buffer that might only last six months in a premium city corridor can comfortably sustain a family for two years in a smaller town, providing ample time to upskill, pivot careers, or wait out the hiring freeze without the crushing pressure of imminent financial ruin.

Navigating this turbulent economic environment requires a fundamental reset of personal finance strategies. The era of assuming constant salary hikes and taking on maximum allowable debt is definitively over. Financial survival now depends entirely on defensive planning and disciplined expense management.

The first major shift is in how down payments are approached. Relying on banks to fund eighty or ninety percent of a property's value is no longer a viable strategy for the salaried class. Anyone considering a real estate purchase must aim to cover at least forty to fifty percent of the total cost upfront through personal savings. Minimizing the total borrowed amount is the most effective way to keep the monthly financial burden manageable.

Secondly, household budgeting must evolve. In dual-income households, it is incredibly risky to base major financial commitments on the assumption that both partners will remain continuously employed. A far safer approach is to ensure that all mandatory fixed expenses—including rent, EMIs, groceries, and insurance—can be comfortably covered by the income of the lower-earning partner alone. The second income should be directed entirely toward aggressive saving, investments, and building wealth.

Building a robust contingency fund is no longer optional; it is an absolute necessity. Standard financial advice typically recommends keeping three to six months of living expenses in liquid form. However, given the prolonged nature of modern job searches in the tech sector, professionals must now aim to build a buffer that covers at least twelve to eighteen months of total outgoings. This fund must be easily accessible and strictly ring-fenced from market volatility.

The ripple effects of this cautious consumer behavior will inevitably shape the future of urban real estate. While top-tier developers continue to push ultra-luxury projects aimed at high-net-worth individuals, business owners, and non-resident Indians, the broader mid-market segment reliant on salaried professionals will have to adapt.

We are likely to see a transition away from speculative price hikes toward a more grounded, steady growth model. Developers may need to recalibrate their offerings, focusing heavily on value-driven projects that offer functional living spaces without the exorbitant price tags attached to excessive luxury amenities. Additionally, as residential leasing becomes the preferred choice for a debt-wary workforce, the rental market might see sustained demand, though landlords will increasingly scrutinize the employment stability of prospective tenants before signing long-term leases.

Ultimately, the current environment serves as a harsh but necessary market correction. It is forcing a re-evaluation of what constitutes financial success. For the modern tech professional, true wealth is no longer defined by the square footage of an apartment or the badge on a car. True wealth is defined by financial resilience, the optionality to navigate career disruptions without panic, and the profound peace of mind that comes from knowing you can survive, no matter what happens tomorrow.