Published On:

June 22, 2026

Updated On:

June 22, 2026

Many homebuyers celebrate massive paper profits when selling their apartments, completely overlooking the steep hidden costs of ownership. Once stamp duty, loan interest, brokerage fees, maintenance, and capital gains taxes are meticulously deducted, your actual real estate returns might be significantly smaller than you originally projected.

The Indian real estate market has always been driven by stories of massive wealth generation. It is highly common to hear anecdotes at family gatherings or office cafeterias about someone who bought an apartment a few years ago and recently sold it for a massive premium. The math usually sounds incredibly simple and highly lucrative. A buyer purchases an under-construction flat in a developing suburb like Noida for ₹1 crore. Fast forward five years, the area develops, infrastructure improves, and the buyer sells that exact same flat for ₹1.8 crore.

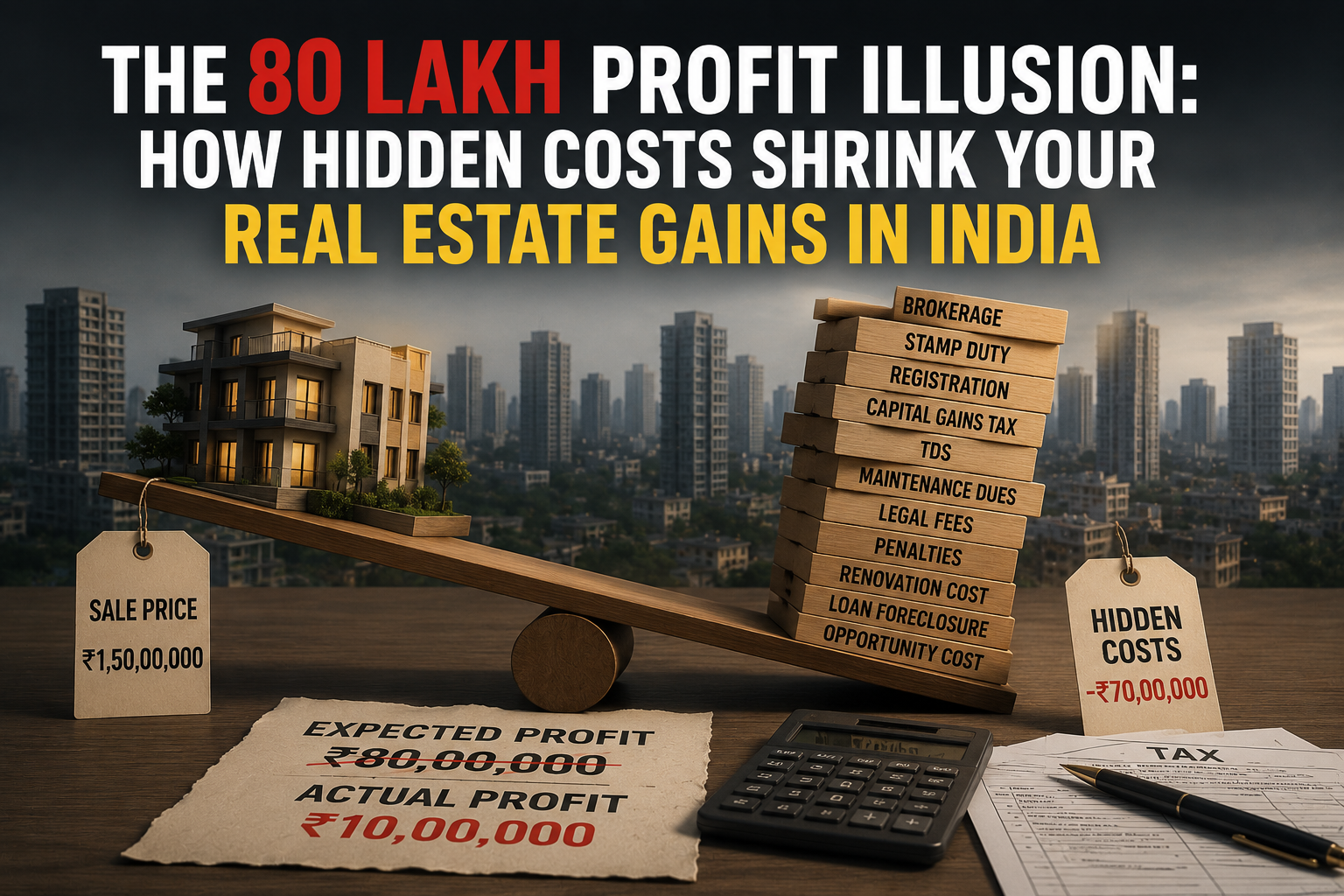

At first glance, this transaction looks like an absolute financial triumph. On paper, the homeowner appears to have generated a cool ₹80 lakh profit in just half a decade. This perceived massive return is what drives thousands of new investors into the property market every single year, hoping to replicate that exact level of capital appreciation.

However, the reality of real estate economics is far more complex. This straightforward calculation represents a massive optical illusion in property investing. Most property owners only compare the initial base purchase price with the final selling price, completely ignoring the massive financial leakages that occur throughout the entire lifecycle of the investment. From the day you decide to buy the property to the day you hand over the keys to the new owner, there is a constant, quiet drain on your capital. When you finally sit down to calculate the hard numbers—deducting taxes, government duties, loan interest, property upkeep, and selling expenses—that ₹80 lakh profit can shrink dramatically, completely changing your actual return on investment.

The financial bleeding begins long before you even receive the keys to your new home. When you see a property listed for ₹1 crore, that is simply the base price demanded by the developer or the seller. To actually acquire the legal rights to that property, you must pay a heavy premium to the state government.

Stamp duty and registration fees are mandatory legal requirements across the country. Depending on the specific state and the gender of the primary owner, stamp duty rates can range anywhere from four to eight percent of the property value, with an additional one percent usually charged as a registration fee. On a ₹1 crore property, this immediately adds up to roughly ₹7 lakh in upfront, non-recoverable cash outflow.

If you happen to be buying an under-construction property, which is usually the preferred route for investors looking for maximum appreciation, the tax burden increases. The government levies a Goods and Services Tax on under-construction residential properties. This typically accounts for another five percent of the property value. That is an additional ₹5 lakh added to your acquisition cost.

Before you even step foot inside your new apartment, your actual cost of purchase has escalated from the advertised ₹1 crore to ₹1.12 crore. You are starting your investment journey in a deep deficit, and the property must appreciate by at least twelve percent just for you to break entirely even on your initial capital outlay. Furthermore, buyers often face hidden developer charges that are rarely highlighted in marketing brochures. These include Preferential Location Charges for units facing a garden or a pool, mandatory clubhouse membership fees, utility connection charges, and exorbitant covered parking fees. In premium projects, these supplementary charges can easily add another eight to ten percent to the overall cost of the property.

Very few people buy real estate entirely with their own liquid cash. The vast majority of property acquisitions are heavily leveraged, relying on home loans distributed by banks or housing finance companies. While taking a loan allows you to acquire an expensive asset with a small down payment, the cost of borrowing is arguably the single largest expense that quietly eats away at your real estate profits.

When calculating their final profit, most sellers conveniently forget to subtract the interest they paid to the bank over the years. To understand the sheer magnitude of this expense, consider a standard twenty-year home loan. At an average interest rate of eight and a half percent, the total amount of interest you pay to the bank over two decades will be nearly equal to the principal amount you originally borrowed. This essentially means you end up paying for the house twice.

Even if you only hold the property for five years before selling, the initial years of a home loan repayment schedule are heavily front-loaded with interest components. If a property’s market value is rising at a conservative rate of five percent annually, but your borrowing cost remains steady at eight and a half percent, you are actually losing wealth in real terms. The appreciation of the physical asset is simply failing to outpace the heavy cost of the capital used to purchase it. When the time comes to sell, the lakhs of rupees paid in interest must be subtracted from the final selling price to reveal the true net gain.

Real estate is a physical, depreciating asset that requires constant financial nourishment to retain its market value. Once you take possession of an apartment, you are immediately locked into paying monthly maintenance charges to the housing society.

During the excitement of buying a home, a monthly maintenance bill of ₹5,000 or ₹8,000 might seem entirely manageable. However, when aggregated over a holding period of five to ten years, this becomes a massive financial burden. A monthly fee of ₹8,000 translates to nearly ₹1 lakh a year, or ₹5 lakh over a five-year period. This is cash that leaves your bank account continuously and yields absolutely no direct return.

There is also a hidden tax implication embedded within housing society fees. If the monthly maintenance charge exceeds ₹7,500 per member, and the housing society has an annual turnover crossing ₹20 lakh, the government mandates an eighteen percent Goods and Services Tax on the entire maintenance amount. This immediately inflates your monthly holding costs.

Beyond standard maintenance, properties suffer from natural wear and tear. Over the years, you will inevitably spend money on civil repairs, plumbing fixes, electrical upgrades, and repainting. Furthermore, when you finally decide to put the property on the market, you cannot simply list it in a dilapidated state. To attract premium buyers and justify your high asking price, you will likely need to invest in a fresh coat of paint, deep cleaning, or minor remodeling. These essential pre-sale repairs can easily drain another two to four lakh rupees from your eventual profit pool.

Unlike stocks or mutual funds, which can be sold with the click of a button for a negligible transaction fee, liquidating real estate is an incredibly expensive, time-consuming, and highly manual process. Finding a buyer willing to pay your target price almost always requires the intervention of a professional real estate broker.

Brokerage fees typically range between one and two percent of the final property transaction value. If you successfully negotiate a sale price of ₹1.8 crore, the broker will expect a commission of at least ₹3.6 lakh for facilitating the deal. This is a massive, immediate deduction from your incoming funds.

In addition to the broker, you will also incur legal fees. Ensuring that the sale agreement is drafted correctly, verifying title documents, obtaining an Encumbrance Certificate, and securing a No Objection Certificate from your housing society all require the expertise of a real estate lawyer. Furthermore, if you are selling a house that still has an active mortgage, your lending bank might penalize you for paying off the loan early. While floating-rate home loans are generally exempt from prepayment penalties, fixed-rate mortgages often attract foreclosure charges that can equal up to one percent of the outstanding loan principal.

After the brokers are paid, the loan is cleared, and the housing society dues are settled, you must finally face the tax department. The government taxes the profit you generate from selling a real estate asset through capital gains taxation. This is often the most severe blow to a seller's perceived profit margin.

If you sell the property within two years of acquiring it, the profits are classified as Short-Term Capital Gains. These gains are directly added to your regular annual income and taxed according to your applicable income tax slab. For high-earning individuals, this could mean surrendering up to thirty percent of the profit directly to the government, alongside applicable surcharges and health cesses.

If you hold the property for more than two years, the profits are classified as Long-Term Capital Gains. Recently, the taxation structure for long-term real estate gains underwent significant modifications, creating a highly complex environment for sellers. Depending on the specific nuances of your purchase date and the newly implemented tax codes, you are generally required to pay a flat tax rate on the profit. In the scenario of our ₹80 lakh paper profit, the capital gains tax liability alone could easily amount to ₹10 lakh, severely diminishing the final cash payout.

While the tax code does offer avenues to save on this tax—such as reinvesting the entire capital gain into another residential property under specific conditions, or locking the funds away in government-issued capital gains bonds for five years—these options severely restrict your financial liquidity. If you actually want to cash out your profit and use it for other life goals, paying the heavy tax is unavoidable.

When you strip away the optical illusion and aggressively factor in every single hidden cost, the financial reality of property investment looks entirely different. Returning to the initial scenario: a buyer purchases an apartment for ₹1 crore and sells it five years later for ₹1.8 crore.

Instead of an ₹80 lakh profit, let us calculate the real math. The buyer paid approximately ₹5 lakh in GST and ₹7 lakh in stamp duty and registration during the purchase. During the sale process, they paid ₹3.6 lakh in brokerage fees to the real estate agent. Finally, the capital gains tax liability wiped out another ₹10 lakh.

Before even accounting for the massive cost of home loan interest, annual property taxes, monthly society maintenance, and the money spent on interior repairs, the transactional costs alone amount to ₹25.6 lakh. The actual net profit has immediately shrunk from the celebrated ₹80 lakh to roughly ₹54 lakh.

Now, consider a slightly different, more extensive scenario often seen in major metros like Mumbai or Bengaluru. A buyer purchases a premium apartment for ₹1.15 crore. After a decade, the property value doubles, and it is sold for ₹2.3 crore. The seller feels wealthy, assuming a gain of over ₹1 crore. However, they spent ₹18 lakh upfront on stamp duty, registration, and initial brokerage. Over ten years, they paid ₹42 lakh in bank loan interest and ₹28 lakh in cumulative society maintenance. They also spent ₹12 lakh over the years on upgrading the kitchen, fixing civil issues, and preparing the house for sale. When these actual cash outflows are calculated, the total expenditure to maintain and sell the asset heavily exceeds ₹2 crore. The massive, life-changing profit they believed they had made barely covers the cost of inflation.

This comprehensive breakdown is not meant to discourage investment in the property market. Real estate remains one of the most stable, tangible, and culturally significant asset classes available. It provides physical security, emotional comfort, and undeniable long-term value. However, the critical takeaway is that buyers must fundamentally change how they evaluate their returns.

Treating real estate purely as a highly liquid, fast-moving financial investment is a dangerous strategy. Affordability goes far beyond calculating whether your monthly salary can cover the EMI. Before making a purchase, smart investors meticulously evaluate the total lifetime cost of ownership. They factor in the non-recoverable government levies, the crushing weight of interest rates over time, the relentless drain of society maintenance, and the heavy transactional friction involved in selling.

By acknowledging and aggressively budgeting for these hidden expenses, you can avoid the dangerous optical illusion of gross price appreciation. Understanding exactly how these costs shrink your gains allows you to make far more accurate financial projections, ensuring that when you finally do sell your property, the money that hits your bank account meets your realistic expectations rather than leaving you with a sense of hidden financial loss.