Published On:

February 10, 2026

Updated On:

February 10, 2026

Young couples are increasingly prioritizing long-term financial security over lavish one-day celebrations, opting to invest wedding budgets into home down payments. This shift allows newlyweds to leverage joint home loan benefits, tax deductions, and compounding asset growth to start their married life on a solid financial footing.

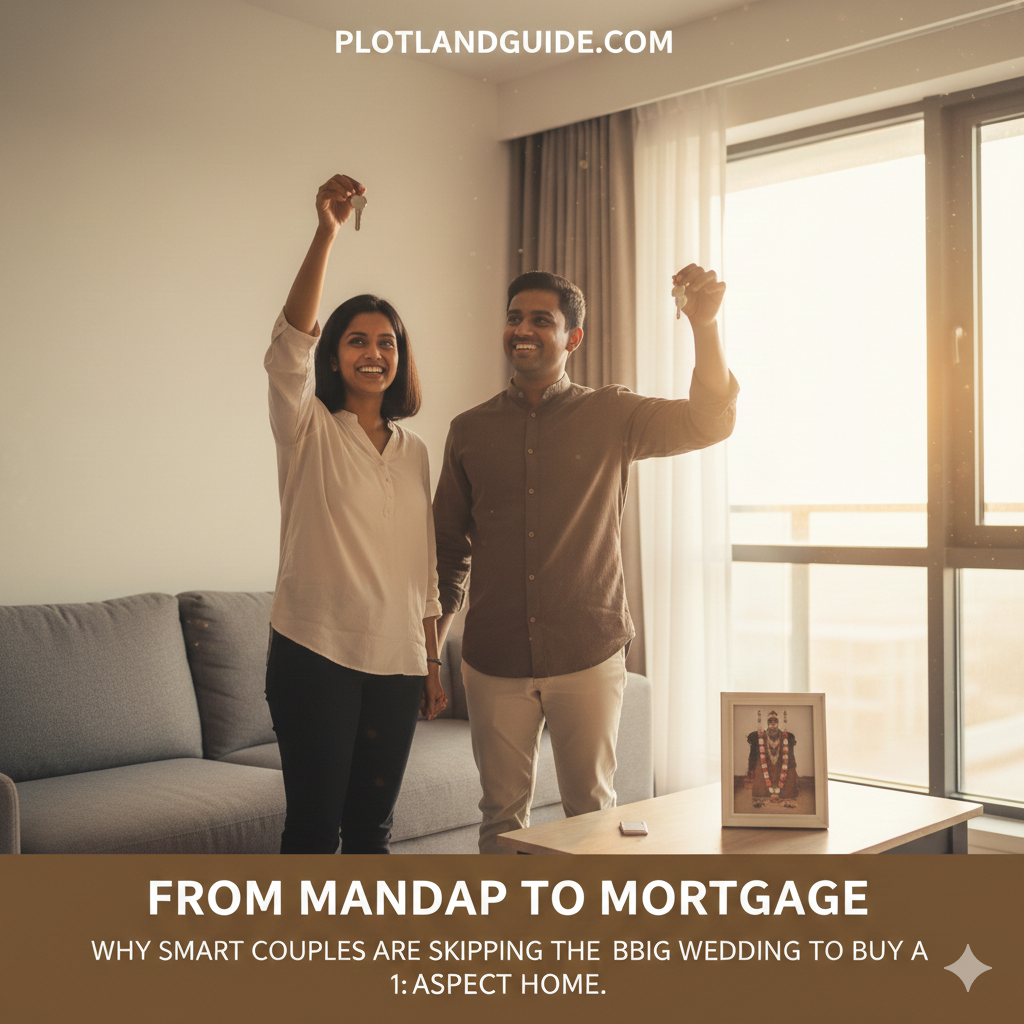

For generations, the "Big Fat Indian Wedding" has been a non-negotiable cultural milestone. It is a day of grandeur, gold, and guests numbering in the hundreds, if not thousands. But for the modern millennial and Gen Z couple, the definition of a "perfect start" is rapidly evolving. Standing at the intersection of skyrocketing real estate prices and equally inflating wedding costs, many young partners are asking a tough but necessary question: Should we spend our life savings on a three-day party, or on a home that lasts a lifetime?

This isn't just a choice between a lehenga and a living room; it is a fundamental clash between social expectation and financial pragmatism. As rental yields tighten and property values in metro cities appreciate, the allure of starting married life with an asset rather than debt is becoming irresistible. This blog explores why swapping the lavish banquet for a brick-and-mortar investment might be the smartest financial move a young couple can make.

To understand why this trend is gaining momentum, one simply needs to look at the numbers. In 2024-25, the average cost of a premium urban wedding easily crosses the ₹30-40 lakh mark. This figure includes venue rentals, catering, jewelry, and logistics—money that is spent once and never returns.

In contrast, that same ₹30 lakh represents a substantial down payment (approx. 20-25%) on a respectable apartment in cities like Bengaluru, Pune, or Hyderabad. By redirecting the "wedding fund" into a "home fund," a couple effectively leapfrogs years of saving. Instead of starting their marriage at zero—or worse, with a personal loan for the wedding—they start with significant equity in an appreciating asset.

One of the most compelling reasons to buy a home as a newlywed couple is the financial leverage of a Joint Home Loan. When you apply for a loan individually, your eligibility is capped by your single income. But when a husband and wife apply as co-borrowers, the bank combines both incomes to calculate eligibility.

This has two immediate benefits:

Additionally, many lenders in India offer a slight interest rate concession (typically 0.05%) if a woman is the primary applicant or co-owner. Over a 20-year tenure, this tiny percentage translates into savings of lakhs of rupees.

Perhaps the biggest unheralded advantage of buying a home together is the tax efficiency. A joint home loan is one of the few financial instruments that offers double tax benefits to a married couple.

Under the current tax laws, each co-borrower who is also a co-owner of the property can claim deductions separately.

When combined, a couple can potentially claim a total tax deduction of up to ₹7 lakh per year. This massive reduction in taxable income can significantly offset the cost of the EMI, making homeownership far cheaper effectively than it appears on paper. For high-earning couples in the 30% tax bracket, these savings are substantial enough to fund a luxury vacation every year—proving that you don't have to sacrifice lifestyle entirely to own a home.

Choosing a house doesn't mean canceling the celebration. The trend has given rise to the "Micro-Wedding"—an intimate affair with 50-80 close friends and family, focused on experience rather than extravagance.

By cutting out the fluff—like obscure distant relatives, 50-item buffets, and designer decor—couples can slash their wedding budget by 60-70%. This "saved" capital becomes the seed fund for their real estate ambition. It is a compromise that honors the tradition of marriage without sabotaging the financial future of the marriage itself.

There is a psychological comfort in entering a marriage knowing you have a roof over your head that is yours. Renting, while flexible, is often viewed by financial planners as paying off someone else's mortgage. In metro cities where rents are escalating by 10-15% annually, the stability of a fixed EMI (which eventually ends) is a hedge against inflation.

Moreover, real estate is a "forced savings" mechanism. A wedding expense is a sunk cost; it has zero residual value. A home EMI, however, builds equity month on month. Five years into the marriage, a couple who chose the house will have a tangible asset worth significantly more than the purchase price, whereas the couple who chose the lavish wedding will only have memories and photo albums.

While the logic is sound, young couples must exercise caution. Buying a home is a 15-20 year commitment, far longer than a wedding reception.

The decision to skip a lavish wedding for a home is not just a financial calculation; it is a maturity test. It signals that the couple values their shared future more than social validation. It prioritizes the "marriage" (the daily life of living together) over the "wedding" (the event).

For young couples standing at this crossroads, the advice is clear: The applause at a wedding lasts for a few seconds, but the security of a home lasts a lifetime. By choosing the latter, you aren't just buying property; you are buying peace of mind, financial freedom, and a solid foundation for your life together.