If you had invested ₹1 crore in 2020, where would that money be today in 2025?

To find out, we compared India’s most popular investment choices — from fixed deposits and gold to mutual funds and various forms of real estate. The results are based on real examples and verified data from investors in Delhi–NCR.

This isn’t theory — these are the kinds of returns people around you have actually earned. The difference lies not just in what they invested in, but how each asset is taxed, compounded, and rewarded over time.

1️⃣ Fixed Deposits — Safe, Predictable, and Tax-Heavy

Fixed deposits are the most common choice for conservative investors. The logic is simple: guaranteed returns and no market risk.

But the hidden cost lies in taxation and inflation.

From 2020 to 2025, the average FD rate hovered around 7% per year.

Now here’s the math:

A ₹1 crore FD at 7% grows to ₹1.40 crore in 5 years before tax.

However, interest is fully taxable at your income slab — for most investors, that’s 30% + 4% cess.

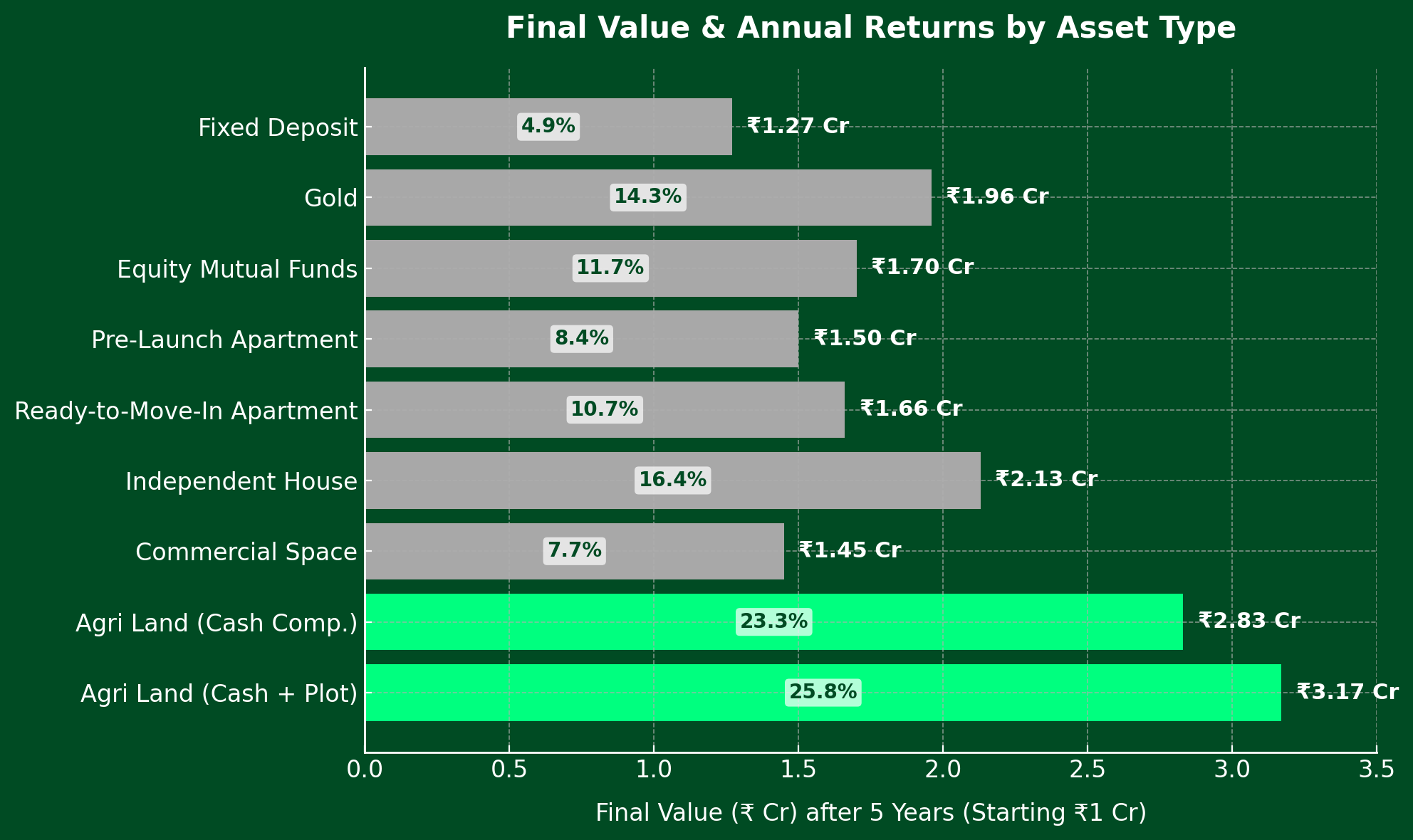

So, your effective post-tax return becomes roughly 4.9% per year, leaving you with only about ₹1.27 crore after five years.

That’s 1.27× growth — safety, yes, but minimal wealth creation.

Inflation quietly eats into the rest.

2️⃣ Gold — A Shining Hedge, Not a Compounder

Gold has long been India’s emotional hedge against uncertainty. Between 2020 and 2025, prices surged sharply due to inflation, geopolitical instability, and currency depreciation — delivering an impressive ~16% CAGR.

If you invested ₹1 crore in gold in 2020:

At 16% annual growth, compounding over 5 years gives you ₹2.1 crore before tax.

Now, when you sell, Long-Term Capital Gains (LTCG) tax of 12.5% (plus cess) applies after 3 years.

After paying tax, your effective post-tax return is ~14.3%, leaving ₹1.96 crore net value.

Gold doubled wealth for many — but it still doesn’t compound income. You hold it, sell it, and pay tax — there’s no recurring yield, no passive return.

So while gold protects purchasing power, it rarely multiplies wealth beyond twofold in 5–6 years.

3️⃣ Mutual Funds (Equity) — The Market Ride

Equity mutual funds are the go-to instrument for long-term capital growth.

Average market performance between 2020 and 2025 hovered around 13% CAGR — impressive, but volatile.

If ₹1 crore was invested in diversified equity funds at 13%, it compounds to ₹1.84 crore before tax in 5 years.

On redemption, equity funds attract LTCG tax of 12.5% (on profits beyond ₹1.25 lakh exemption).

That cuts effective returns to ~11.7% net, giving you about ₹1.70 crore post-tax.

This is 1.7× growth — respectable, but the risk-reward balance depends entirely on market cycles and timing. The volatility may not suit everyone, but the returns have historically beaten inflation comfortably.

4️⃣ Apartments (Pre-Launch) — The Patience Test

Real estate pre-launch projects promise high returns — if they ever deliver.

Take this real case:

A family friend booked Amrapali Dream Valley, Greater Noida in 2010 at ₹1,500/sq ft.

Possession came only in 2025 — 15 years later — at a current market rate of ₹6,000/sq ft.

Let’s translate that: the property appreciated 4× over 15 years, implying an average annual return of 9.6%.

If the same ₹1 crore were invested in 2020 at 9.6%, it would grow to ₹1.58 crore before tax.

After 12.5% LTCG on property gains, your net return becomes 8.4%, bringing your final amount to ₹1.50 crore.

The lesson? Pre-launch properties sound lucrative, but delays, legal hurdles, and financing risks often erode compounding. The longer the wait, the lower the real yield.

5️⃣ Apartments (Ready-to-Move) — Safer, Steadier Growth

Now contrast that with a ready-to-move property — where both rental yield and price appreciation kick in immediately.

Example:

A relative bought a flat in Golf City Homes, Sector 75, Noida, in 2018 at ₹4,500/sq ft.

By 2025, the rate touched ₹11,000/sq ft — nearly 2.4× growth in 7 years.

That’s roughly 12.2% annual return. After 12.5% LTCG, your net effective return is about 10.7%.

If ₹1 crore were invested in 2020 and grew at 10.7% annually, it would be ₹1.66 crore by 2025.

You also enjoy rent (typically 2–3% annually), adding a passive layer of return.

Ready properties balance safety with liquidity — ideal for those seeking stability and decent compounding.

6️⃣ Authority-Allotted Independent House — Clear Titles, Clear Gains

Authority-allocated plots are one of NCR’s best-kept secrets in wealth creation.

Take this verified example:

A family member purchased a 220 sq m Noida Authority plot in 2010 for ₹26 lakh, plus ₹10 lakh for constructing the ground floor — a total of ₹36 lakh.

By 2025, the property’s market value stands near ₹4 crore.

That’s a 15-year CAGR of around 18%, and after deducting 12.5% LTCG, net effective return ~16.4%.

If ₹1 crore was invested in 2020 and compounded at this rate for 5 years:

It would grow to ₹2.13 crore, roughly 2.13× your capital.

Authority plots provide legal assurance, planned infrastructure, and consistent appreciation.

They quietly outperform apartments because the underlying land value drives growth — not just construction quality.

7️⃣ Commercial Space — Income with Uncertainty

Commercial assets combine rental yield with appreciation potential — but both depend heavily on occupancy and market demand.

For instance, a friend invested in NX One, Greater Noida, in 2013 at ₹2,700/sq ft.

Today, rates hover around ₹7,000/sq ft — 2.6× growth in 12 years.

That’s roughly 8.8% annual appreciation. After 12.5% LTCG, you’re left with ~7.7% effective return.

If ₹1 crore was invested in 2020 at 7.7%, it becomes ₹1.45 crore by 2025.

Commercial properties can deliver stable rent (6–8% yields) if leased, but vacancy risk and maintenance often offset returns. They perform best during expansion cycles, not slowdowns.

8️⃣ Agricultural Land (Cash Compensation Only) — The Tax-Free Multiplier

Now comes the game changer — agricultural land acquired by development authorities like YEIDA or Noida Authority.

Example:

In 2005, a family bought 4 bighas in Noida for ₹10 lakh.

In 2013, the Authority paid ₹57 lakh as compensation.

This translates to a 23.3% annual return over 8 years — and here’s the kicker:

Under Section 10(37) of the Income Tax Act, compensation from compulsory acquisition of agricultural land is 100% tax-free if certain conditions are met.

If ₹1 crore were invested in 2020 and compounded at this same 23.3%, it would be ₹2.83 crore by 2025 — completely tax-free.

That’s why authority-linked agricultural plots near major projects like Jewar Airport have created quiet millionaires. No tax, no speculation — just structured land value escalation.

9️⃣ Agricultural Land (Cash + Free Plot) — The Hidden Wealth Engine

Here’s the most powerful example of all.

In 2006, a family friend bought 2.5 bighas in Noida for ₹10 lakh.

When the land was acquired in 2021, he accepted a lower ₹60 lakh cash compensation instead of a higher amount — because the Authority also offered a free developed sector plot (Naksha 11 scheme).

He sold that free plot the same year for ₹2.6 crore.

In total, ₹10 lakh became ₹3.2 crore in 15 years.

That’s an average annual return of 25.8%, and again, fully tax-free because compensation and allotment fall under exempt categories.

If ₹1 crore had been invested in 2020 at 25.8%, it would be ₹3.17 crore by 2025 — 3.17× growth in just 5 years.

These hybrid compensation models — cash + free plot — are unique to YEIDA and Noida Authority. They combine liquidity and long-term appreciation in one event.

Quick Comparison — Same ₹1 Crore, Different Destinies

💡 The Takeaway: Returns Create Income, But Land Creates Legacy

Same ₹1 crore.

Same 5 years.

Different choices — drastically different outcomes.

Fixed deposits give comfort. Mutual funds give growth.

But authority-backed land investments near Noida Airport, Tappal–Bajna, and YEIDA sectors deliver both — appreciation and exemption.

- Tax efficiency: Agricultural compensation is fully exempt under Section 10(37).

- High compounding: 18–26% CAGR with structured government acquisition and infrastructure plans.

- Legacy potential: Land near airports, expressways, and master-planned zones compounds generationally.

Some earned returns.

Few earned income.

But the rare ones — they built generational wealth.

About PlotLandGuide

PlotLandGuide is a research-driven real estate advisory specializing in high-growth farmland, Naksha 11, and residential investment opportunities around the Noida International Airport (Jewar) and YEIDA region.

With 25+ years of legacy and over 100 investors served, PlotLandGuide helps families build structured, tax-efficient wealth through land investments that grow faster, safer, and smarter than traditional options.